Consolidation loan

Reduce your repayments by paying off old loans – even with a negative Schufa rating

Fixed nominal interest rate of 2% for the entire loan term. Effective annual interest rate: 2%. Net loan amount: EUR 2,000 to 200,000. Loan duration: 6 to 120 months. Example: Fixed nominal interest rate of 2% for the entire loan term. Effective annual interest rate: 2%. Net loan amount: EUR 25,000. Loan duration: 72 months. Monthly payment: EUR 369. Total interest: EUR 1,568. Total payment: EUR 26,568.

Consolidation loans: Important information at a glance!

What is a consolidation loan?

Anyone can get into debt. Sometimes you go into debt intentionally, like when you take out a loan to buy a house, but sometimes debt arises out of necessity. For example, if you had to pay for an expensive car repair and used your bank account to overdraw, it was not intentional at all – and it was not your fault at all!

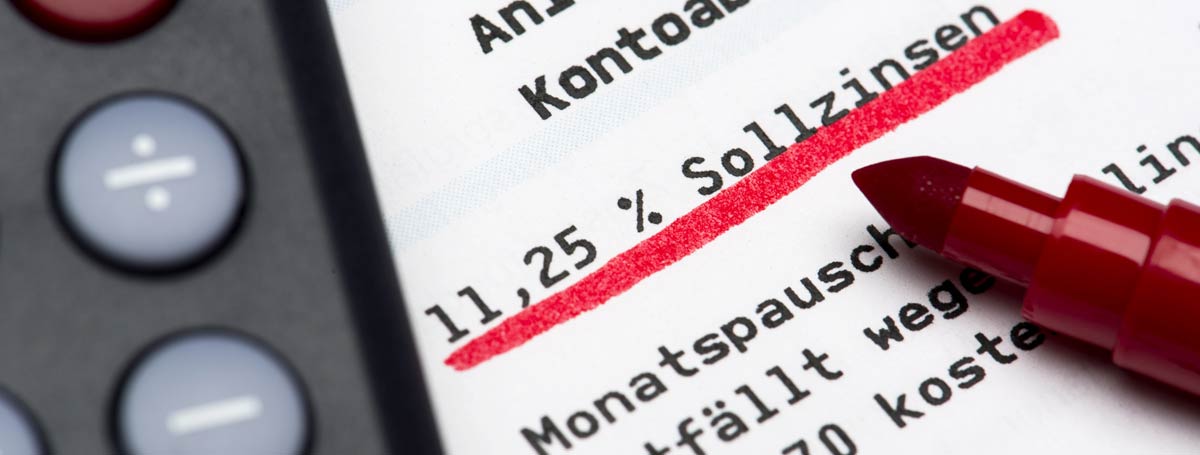

The main problem with overdrafts is the subsequent costs . Unlike traditional installment loans, the interest rate on overdrafts is quite high. Ultimately, this means: the longer you wait to pay off the negative balance in your account, the more expensive it will be for you!

A similar situation can occur with other loans. The cost of a loan depends on the interest rate, which can change quickly. Interest rate developments are largely influenced by decisions of the European Central Bank (ECB). Simply put, the base rate determines how high the interest rate on a loan will be.

The good news is that interest rates are currently low – that’s bad for savers, but good for people like you who are looking for a cheap consolidation loan! Debt consolidation takes advantage of low interest rates to pay off an old and overpriced loan with a higher interest rate.

Multiple loans can also be refinanced with a consolidation loan . The current low interest rates can be a great advantage, especially for those who are paying off an expensive loan in installments or who need to settle their overdraft! This is possible thanks to the aforementioned consolidation loan, which allows you to get new funds to repay old debts - and thus save a lot of money.

Consolidation loan: important benefits and conditions!

Essentially, a consolidation loan is nothing more than a traditional installment loan . The only difference is its purpose : as the name suggests, a consolidation loan works to consolidate debts in order to save money through lower interest rates and significantly reduce your monthly financial burden. This also frees up funds that you can better use for other things and desires!

However, it is not possible to say exactly how much money you can save. It depends on a number of factors. First, you need to know the balance or cost of your old loan. To do this, you need to know the remaining term , effective annual interest rate and monthly payment of your current loan. Second, you need to know the cost of the loan and the monthly payment of the consolidation loan. To do this, you also need to know the term and effective annual interest rate, which can be used to calculate the cost of the loan and the monthly payment.

The benefits of consolidation loans at fluxcreidi.com in a nutshell

Improve your credit rating!

If you are able to reduce the number of loans you have to one by consolidating your debts, this will usually improve your credit score!

Get rid of debt faster!

If you combine multiple loans into one consolidation loan, you have the option to set new terms. For example, if your income situation has improved since your last loan application, you can increase your monthly payment and/or shorten the repayment period . This way, you will get rid of debt faster!

Take care of your financial situation!

Having to track just one consolidation loan rather than several individual loans makes it easier to monitor your financial situation, giving you a better overview and estimate of your monthly financial burden.

You have more money available!

If a consolidation loan is cheaper than your current loan, meaning lower interest rates, that means you have more money available each month and the opportunity to fulfill new dreams!

Debt restructuring: the best advice from experienced financial experts

There are often many misconceptions about loan consolidation. The entire process, from application to payment, is often easier and faster than many people think – especially with us at fluxcreidi.com!

Especially with today's interest rates, debt consolidation is likely to pay off, and for many, a consolidation loan will reduce their monthly financial burden . With interest rates currently at historic lows, there's no better time to refinance than now.

That's why we've gathered some valuable tips on debt restructuring below.

Tips and tricks for an affordable consolidation loan

Tip 1: Balance your overdraft by restructuring your debt

Interest rates on current account overdrafts are usually much higher than those on installment loans, regardless of the bank. This is a significant financial burden for you.

Therefore, it almost always makes sense to balance an overdraft with a consolidation loan, which could mean saving hundreds of euros in a short time.

Tip 2: Consolidate loans and improve your credit score

Financial viability largely depends on your creditworthiness, or your Schufa score. However, the number of loan agreements you currently have also has a negative impact on your Schufa score - unfortunately, usually.

Therefore, consolidation loans are a great way to pay off old loans or merge them into one loan. This improves your Schufa score and even gives you the opportunity to get approved for a new loan if you need new funds.

Tip 3: Stop being afraid of balloon financing

Balloon financing is often offered for car financing. After the installments, there is often a final payment at the end of the term, which many people cannot afford.

With a consolidation loan, you can solve this problem by paying the last installment on the new loan , and in a way, financing it yourself!

Tip 4: Don't forget the bank's early repayment fee

While it is generally true that refinancing is always worthwhile if the effective interest rate of the refinanced loan is lower than the interest rate of the existing loan, this is only half the truth. Since banks lose revenue when they repay an existing loan early, they often charge a so-called early repayment fee .

You can find out the amount of this fee in your current loan agreement, but it varies greatly from bank to bank. The average early repayment fee is 1%. So refinancing is worth it – in most cases – even if your bank charges a prepayment fee.

How to refinance a loan properly: See how to do it!

Overview of total debt

First, you should look at your current debt . This doesn't just include your current loans. It can also include credit card debt. This will give you an idea of your monthly financial burden , which could be causing you to go into debt.

Compare loan terms

Applying for a personal debt consolidation loan

Apply for a consolidation loan

Repaying loans through debt consolidation – frequently asked questions

-

What happens during debt restructuring?

In debt consolidation, your existing loans are paid off and replaced with a new, more affordable loan. You take out a new loan to pay off all of your old loans at once. Therefore, the loan amount in your new agreement will be at least equal to the balance you owe to your previous creditors. The new bank will automatically transfer the amounts you owe to the old banks. Depending on the terms of the agreement, you may also receive a payment in your account for your own use. The new loan amount is then calculated based on the outstanding balance and the additional amount required.

-

When is it worth restructuring debt?

Refinancing is worth it if the annual effective interest rate on the new loan is significantly lower than the interest rate on the old loan. Even a difference of 0.2 to 0.3 percent will be an advantage to you when refinancing the loan. If you want to repay multiple loans, the interest savings should be applied to all of the old loans. Therefore, refinancing is only worth it if the repayment "covers" all of the loans.

-

When does it make sense to refinance a loan in installments?

If you need to pay lower interest rates on the new loan than on the existing loan, it makes sense to refinance the loans in installments. Another advantage is that you only have to pay one installment to the bank on a given date. If you pay off several loans at the same time, it is much easier for you to replace them with one, cheaper loan. After refinancing, you will only have one current loan.

-

How can I refinance my debt?

With debt consolidation, you can merge your old loans and pay them off with a new one. You only pay one payment to the bank and save money thanks to lower interest rates. To consolidate your debt, you need a new loan that is at least equal to the balance. For debt consolidation to be worthwhile, the new contract must have a lower annual percentage rate than your previous financing. You have the best chance of getting a good loan by comparing loans, such as those offered for free by Fluxcreidi. Simply enter “debt consolidation” as the purpose of your application and the balance of your old loans as the loan amount. Our loan specialists will then find you the best offer and take care of the entire process.

-

How often can you refinance?

In principle, you can refinance as often as you like, provided you get the bank's permission each time. Refinancing basically means taking out a new loan to replace the old one. It makes sense to repay your existing loan if you get a better interest rate on the new loan. There are no requirements or legal provisions that set a maximum refinancing amount.

-

Can a bank refuse debt restructuring?

Whether a bank can refuse debt consolidation depends on the details of the contract. First, debt consolidation is essentially a new loan. Therefore, you have to submit a loan application, which can be refused – just like any other application for financing. However, if you are approved for a new loan, your old bank cannot immediately refuse debt consolidation. They may, however, adhere to notice periods. A prepayment fee may also be charged. Read the details in your existing loan agreements before signing a new agreement.

-

How does a loan increase work?

A line of credit works basically like any other loan, as a new loan agreement involves a new credit check from the bank. Strictly speaking, this does not increase the amount of your existing loan. Instead, you take out a new loan from the bank. You can continue to use this second loan at the same time as the first one, or you can use the line of credit to consolidate your debt. In this case, the new loan is your remaining debt plus the additional loan amount. The bank will pay off the old loan in one lump sum and make the remaining amount available to you for use.

-

Can you refinance an existing loan?

Yes, it is possible to top up an existing loan. However, technically, it is a new loan. It is arranged in addition to the existing loan or replaced with the old contract as part of a debt consolidation. In both cases, new approval from the bank is required. So, if you want to top up an existing loan, you will still need to provide proof of your salary and bank statements.

-

Can you get more loans?

Yes, you can get multiple loans. The determining factor is your financial capacity as a borrower – and therefore the question of whether your income is sufficient for more than one loan repayment. In general, the higher your income, the more likely you are to get multiple loans at the same time. However, the determining factor is how much money you have available each month after all expenses have been deducted. If there is enough room for repayment and interest payments, the bank may approve multiple loans.

-

Can loans be consolidated?

Yes, you can combine loans. This is called debt consolidation because it replaces your existing loans with a new loan. After consolidating your loans, you no longer make multiple payments to different lenders, but instead make one payment. This can save you money because the new payment is usually lower than the sum of your previous monthly payments. The savings come from a lower annual percentage rate. By the way, you can not only combine traditional loans, but also other installment payments, dealer financing, etc.

-

Is it possible to consolidate two bank loans?

Yes, you can consolidate two loans with a bank if the bank allows it. Both loans do not have to be provided by the same bank. Precisely, during consolidation, the existing loans are repaid in one go – from the proceeds of the new loan. So, when you consolidate your existing loans, you get a new loan. The benefits are lower interest rates, lower monthly payments and greater clarity, as you only pay one monthly payment to one bank.

-

How can I balance my overdraft?

With an overdraft, the bank gives you the option to overdraw your account. This allows you to spend more money than is available in the account. The bank charges interest, which is often very high. This is not a big problem if the overdraft is only used for a short period of time and is repaid with the next paycheck. However, many consumers have a permanent negative interest rate on their account and therefore pay very high interest rates on the overdraft for months or even years. In such a case, it is strongly recommended to repay the overdraft. If you cannot increase your income and reduce your spending, an installment loan is considered the best way to restore the balance in the account. That is why you take out a loan to repay the overdraft. This makes sense because the interest rate on an installment loan is much lower than the interest rate on an overdraft. The loan amount is transferred directly to your bank account. The overdraft is therefore repaid immediately and from that point on, interest on the overdraft is no longer calculated. And depending on the loan amount, you will also have a comfortable financial reserve in your account, which can protect you from being in the red again, even in the event of unexpected expenses.

-

How bad is it to overdraw your account?

Overdrafting your account is not a problem if it is only a short-term overdraft. Banks offer overdraft loans for such situations. Overdrafts should usually be repaid by the next payday at the latest. If this cannot be done, there is a risk that the account will be permanently overdrawn. Although this is not prohibited, if you have an appropriate contract with the bank, it can be very expensive. Many banks charge very high interest rates on overdrafts. Therefore, before you overdraw your account for months or even years, it is better to get an installment loan and use it to pay off the balance. The interest rates on installment loans are much lower than those on overdrafts, so you can save a lot of money this way.

-

How quickly can I repay my overdraft?

When it comes to the question of how quickly you should pay off your overdraft, there is only one answer: as soon as possible. An overdraft is not a long-term financial instrument, but is only intended for short-term financial problems. An overdraft should be repaid within six to eight weeks at the latest. If that doesn't work, the motto is: act quickly and repay the overdraft immediately with an installment loan. Regular loans with a maturity period of twelve to 48 months have much lower interest rates than overdrafts. This way, you can pay off the overdraft quickly and avoid the debt risk due to high interest rates on overdrafts.

-

What should you do if you have a deficiency?

If you have a negative balance, you should try to balance your account as soon as possible. Ideally, this should be achieved as soon as your next payday arrives. If your salary is not enough to get you out of a negative balance, you need other options: Do you have a balance in another account that can be transferred to your bank account? Can friends and family help you in the short term? If the answer to both of these questions is "no", an installment loan may be the best solution. The main problem when you have a negative balance is the high interest rates on overdrafts. These make it difficult to overdraft again. That's why financial experts recommend installment loans as an alternative. The actual interest rates are much lower here. The loan amount is transferred directly to your account, which means you are immediately out of a negative balance. The difference between the loan amount and the previous negative balance remains in your account as a credit - preventing you from going back into a negative balance.

Service

Fixed nominal interest rate of 2% for the entire loan term. Effective annual interest rate: 2%. Net loan amount: EUR 2,000 to 200,000. Loan duration: 6 to 120 months. Example: Fixed nominal interest rate of 2% for the entire loan term. Effective annual interest rate: 2%. Net loan amount: EUR 25,000. Loan duration: 72 months. Monthly payment: EUR 369. Total interest: EUR 1,568. Total payment: EUR 26,568.